Insurance Coverage for Mold Remediation in Toronto: What You Should Know

When mould is discovered in a Toronto home, one of the first questions homeowners ask is whether their insurance will cover the cost of dealing with it. It’s a reasonable and important question — professional mould remediation is a significant investment, and understanding what your policy does and doesn’t cover can shape the decisions you make about how and when to act.

The honest answer is that it depends. Mould coverage under a standard home insurance policy in Ontario is not straightforward, and many homeowners are surprised to discover that a problem they assumed was covered is not — or that coverage exists but comes with conditions they weren’t aware of. Understanding the landscape before you file a claim can save you from costly misunderstandings and help you navigate the process more effectively.

This post is intended to help Toronto homeowners understand the general principles around insurance and mould remediation. It is not legal or insurance advice, and the specifics of your situation will always depend on the exact terms of your individual policy. When in doubt, speak directly with your insurer or a licensed insurance broker.

The Core Principle: Cause Matters More Than the Mould Itself

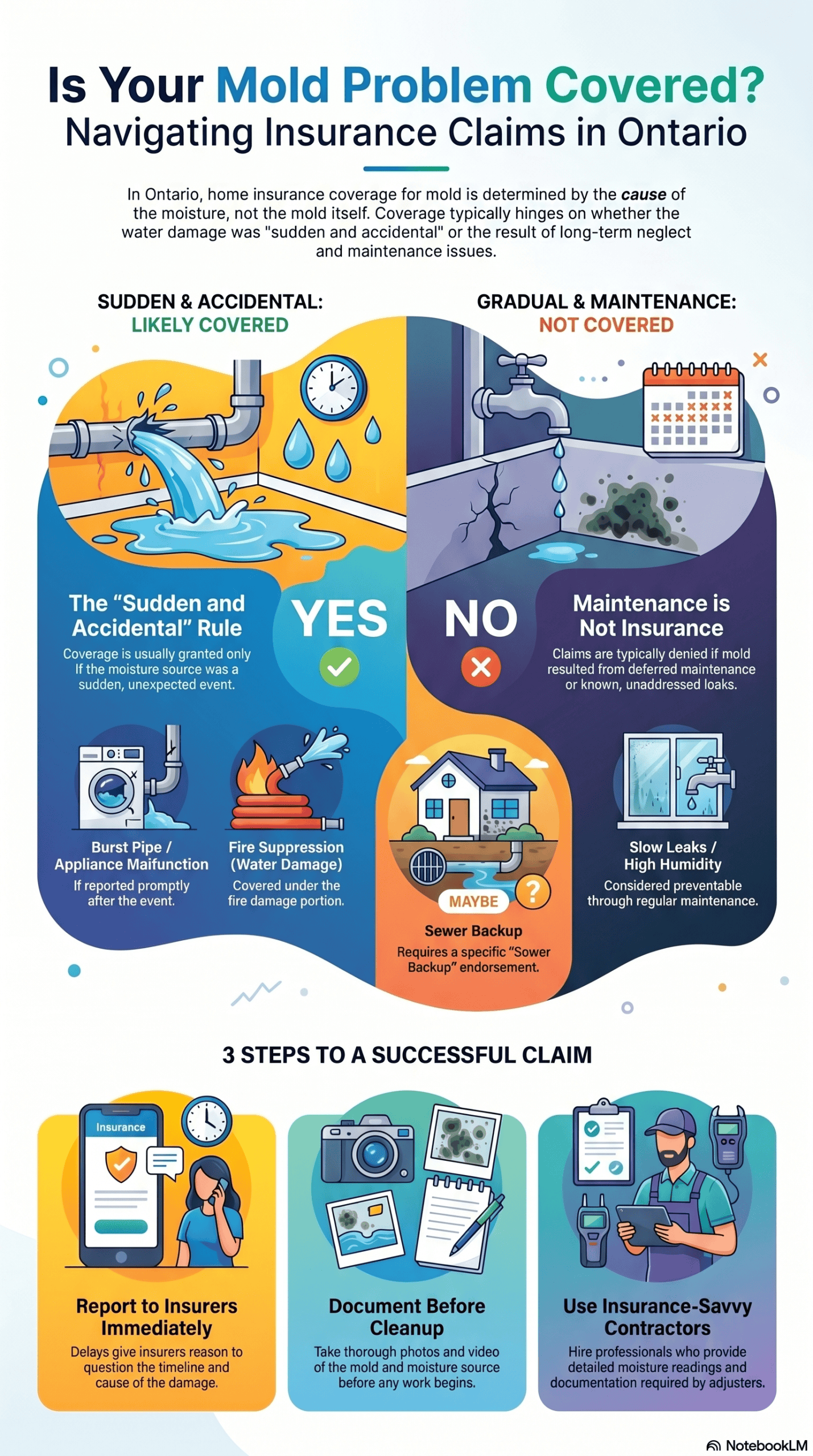

Home insurance policies in Ontario are generally structured around the concept of sudden and accidental loss. The cause of the damage — not the damage itself — is what determines whether a claim is covered.

This distinction is critically important when it comes to mould, because mould is almost never the original event. It is a consequence of moisture. Whether that mould is covered by your insurance typically depends on whether the moisture source that caused it was itself a covered event.

In simple terms: if the water event that led to the mould is covered by your policy, the resulting mould remediation is often covered as well. If the water event is not covered — or if the mould developed as a result of a condition that was long-standing and unaddressed — coverage is typically not available.

When Mould Remediation Is Likely to Be Covered

Sudden and Accidental Water Damage

If mould develops as a direct result of a sudden, accidental water damage event — a burst pipe, an appliance malfunction, an accidental overflow — and the mould is discovered and reported in a timely manner, most standard home insurance policies in Ontario will cover the remediation as part of the broader water damage claim.

The key word here is sudden. Insurance is designed to protect against unexpected events, not gradual deterioration. A pipe that burst overnight and saturated a wall, leading to mould growth discovered within days or weeks, is a very different situation from a slow drip that has been present for months without being addressed.

Fire Suppression Water Damage

When a home is damaged by fire and extinguished with water — whether by sprinkler systems or firefighting — the resulting water damage and any subsequent mould growth is generally covered under the fire damage portion of a standard policy.

Roof Damage from a Sudden Event

If a storm causes sudden physical damage to a roof — a fallen tree, wind damage, hail — and water enters through the damaged area, leading to mould growth in the affected space, that mould remediation is typically covered as part of the storm damage claim. The important qualifier is that the roof damage itself must be the result of a sudden event, not pre-existing deterioration.

Sewer Backup — With the Right Coverage

Mould resulting from a sewage backup event can be covered, but only if your policy includes sewer backup coverage. As noted in our sewage cleanup guide, this is typically an add-on endorsement to a standard Ontario home insurance policy — it is not included automatically. If you have this endorsement and a backup event leads to mould growth, your remediation should fall within the scope of that coverage.

When Mould Remediation Is Typically Not Covered

Long-Term or Gradual Moisture Problems

This is where most coverage disputes arise. If mould has developed over an extended period as a result of chronic moisture — a slow leak that was ignored, persistent basement seepage, ongoing condensation — insurance companies will typically deny the claim on the basis that the underlying condition was not sudden or accidental, and that it could or should have been addressed before mould developed.

Insurers may investigate the history of a moisture problem when a mould claim is filed, and evidence that a homeowner was aware of the issue — a past repair, a previous complaint, a prior inspection report — can be used to support a denial.

General Humidity and Condensation

Mould that develops due to high indoor humidity, poor ventilation, or condensation — without any specific sudden water event — is generally not covered under standard home insurance. These are conditions that insurers consider to be within a homeowner’s control through regular maintenance and moisture management.

Flood Damage

Overland flooding — water entering a home from rising rivers, lakes, or storm surge — is not covered under standard Ontario home insurance policies. Overland flood coverage is a separate product that must be specifically added to a policy, and it is not universally available in all areas. Mould resulting from an overland flood event would only be covered if this additional protection is in place.

Maintenance-Related Issues

If mould is determined to have resulted from deferred maintenance — a roof that was known to need repair, a foundation crack that was visible and unaddressed for years, plumbing that was aging and known to be problematic — coverage will typically be denied. Home insurance is not a maintenance contract, and insurers take the position that a homeowner who fails to maintain their property has not met their obligations under the policy.

How to Give Yourself the Best Chance of a Successful Claim

Understanding how insurers evaluate mould claims helps you take the right steps from the moment a problem is discovered.

Report Promptly

Delays in reporting a water damage event or mould discovery can complicate or jeopardize a claim. Most policies require prompt notification of a loss, and a significant gap between when damage occurred and when a claim is filed gives insurers reason to question the timeline and circumstances.

If you discover water damage or mould, contact your insurer as soon as possible — even if you aren’t yet certain whether the loss is covered.

Document Everything Before Cleanup Begins

Before any extraction, removal, or cleanup begins, take thorough photographs and video of the affected area. Capture the extent of the damage, the location of visible mould, any obvious source points, and the condition of surrounding materials. This documentation is essential to supporting your claim and establishing the scope of the loss.

Once cleanup and remediation begin, that visual evidence is gone. You cannot recreate it after the fact, and adjusters reviewing a claim without it have less to work with when assessing coverage.

Use a Restoration Company Familiar With the Claims Process

Working with a restoration contractor who understands how insurance claims work — and who documents their scope of work, moisture readings, and remediation process in the detail that insurers require — makes a meaningful difference in how a claim is handled.

A contractor who provides vague invoicing, fails to document moisture readings before and after drying, or doesn’t communicate clearly with your adjuster creates gaps in the record that can complicate the claims process. A contractor experienced in working directly with insurers knows what documentation is needed and produces it as a standard part of the project.

Understand Your Policy Before You Need It

The best time to understand what your home insurance covers is before a problem occurs. Review your policy with your broker — specifically asking about water damage coverage, sewer backup endorsements, overland flood coverage, and any mould-specific exclusions. If there are gaps in your coverage that concern you given the age or condition of your home, now is the time to address them.

Toronto homeowners in older properties, homes with aging plumbing, or areas prone to basement flooding and sewer backup events are particularly well-served by reviewing and strengthening their coverage proactively.

Working With Your Adjuster

When a mould remediation claim is active, you will typically be assigned an insurance adjuster whose role is to assess the claim on behalf of your insurer. Understanding how to work effectively with your adjuster can help the process go more smoothly.

- Be factual and specific when describing how and when the damage was discovered. Stick to what you know and avoid speculation about causes or timelines you aren’t certain of.

- Provide all documentation promptly — photos, moisture readings, contractor assessments, and any prior inspection reports that are relevant.

- Ask questions if you don’t understand what’s being covered, what’s being excluded, or what the basis for a determination is. You have the right to understand your claim.

- Work with your restoration contractor to ensure their scope of work and invoicing is aligned with what the adjuster has approved before work proceeds.

If a claim is denied and you believe it should be covered, you have the right to dispute the decision — first through your insurer’s internal appeals process, and if necessary through the General Insurance OmbudService (GIO), which is an independent dispute resolution service available to Ontario consumers at no charge.

Restoration Mate Works Directly With Insurance Providers

Navigating an insurance claim while also managing the stress of a mould problem in your home is a lot to handle at once. Restoration Mate works directly with all major insurance providers across our service locations, and our teams understand the documentation, communication, and process requirements that support a successful claim.

From the initial assessment and moisture investigation through remediation, structural drying, and full reconstruction, we document every stage of the project in the detail insurers require — and we communicate directly with adjusters on your behalf so you’re not left managing that relationship alone.

If you’re dealing with mould in your Toronto home and have questions about how the insurance process works alongside remediation, our team is available to help — any time of day or night. Contact us today to schedule a free estimate.

Leave a Reply

Want to join the discussion?Feel free to contribute!